The Cash Drag Dilemma: Balancing One-Time Windfalls with Monthly Investing

Read Time:7 Minute, 3 Second

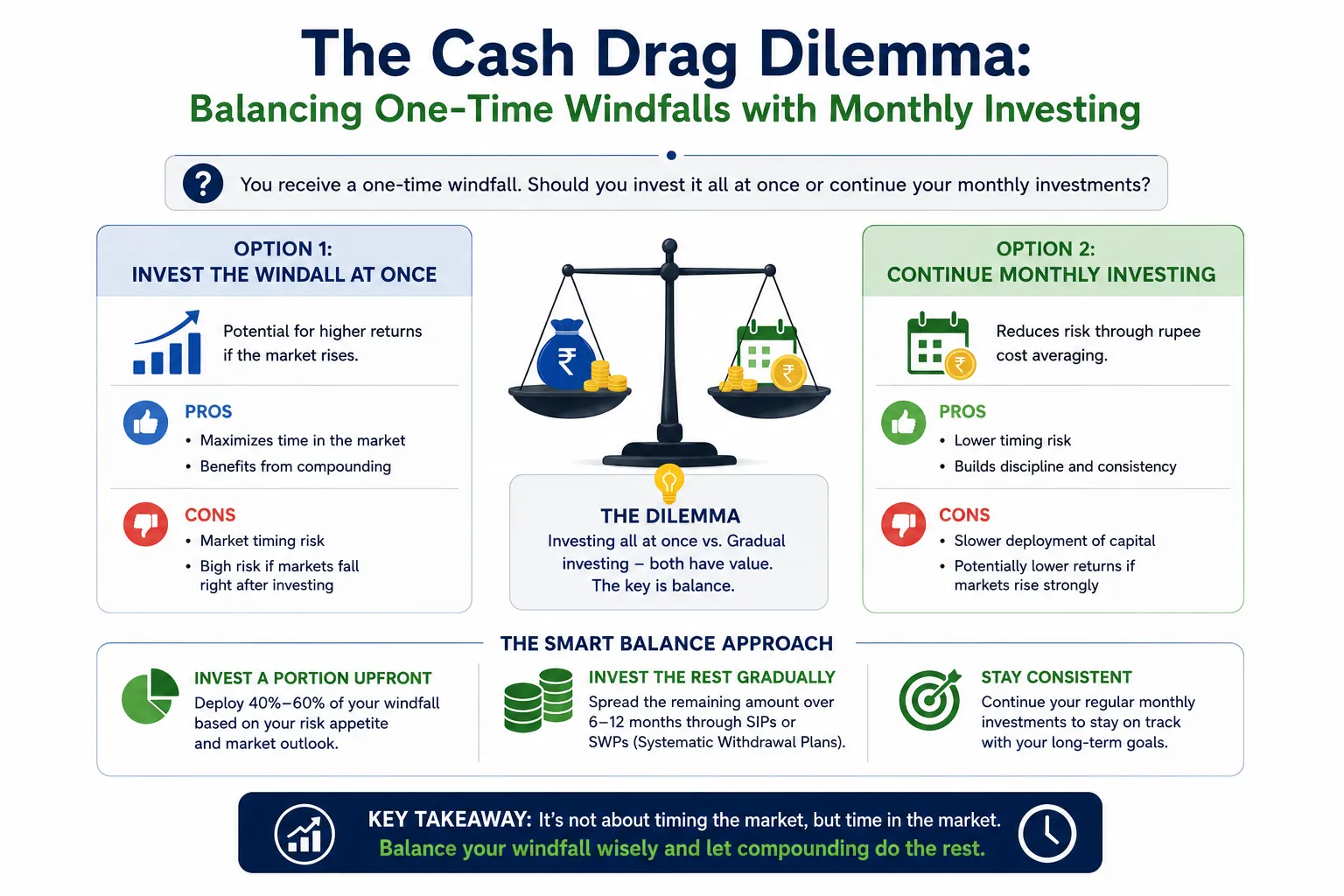

Let’s be completely honest about a situation that sounds like a great problem to have, but is actually incredibly stressful. You suddenly find yourself with a large amount of cash. Maybe you received a massive year-end corporate bonus, sold an ancestral property, or finally had a few large fixed deposits mature.

Common sense tells you to invest it so it can grow. But when you look at the stock market, you freeze. You worry that the market is sitting at an all-time high. You are terrified that the exact day you invest your hard-earned money, the market will crash, wiping out lakhs of rupees overnight. So, you do nothing. You leave the money sitting in a basic savings account, telling yourself you will wait for the “right time” or a “market dip” that never seems to arrive.

This hesitation is entirely normal. I hear this fear all the time, and your anxiety about losing money is completely valid. However, while your cash sits idle in a savings account, it is suffering from what financial experts call “cash drag.” Inflation is quietly eating away its actual purchasing power every single day.

To break out of this paralysis, you need a strategy that protects your peace of mind while keeping your money productive. This requires blending two different investment styles. By understanding how to use a sip calculator alongside a lumpsum calculator, you can build a highly structured, emotion-free blueprint for your wealth.

The Lumpsum Reality: Mathematics vs. Human Emotion

When you have a large chunk of money, the most mathematically efficient thing to do is to invest it all at once. This gives your capital the maximum possible time to grow.

If you open a lumpsum calculator and run the numbers, the math is undeniable. Let’s say you have ₹15,00,000 from a property sale. If you invest that entire amount on day one into a solid index fund that averages a 12% annual return, and you leave it alone for 15 years, the calculator shows your money could grow to over ₹82,00,000. The spreadsheet tells you to dump all the money into the market today and walk away.

But you are a human being, not a spreadsheet.

The stock market does not move in a straight, predictable upward line. It is highly volatile. If you invest that ₹15 Lakhs today, and a global economic panic causes the market to drop by 10% next week, your portfolio will immediately show a loss of ₹1.5 Lakhs. For most retail investors, seeing that kind of red on their screen triggers intense panic. The emotional pain of losing money is far stronger than the joy of making it. This panic often causes people to pull their money out at the absolute worst time, turning a temporary paper loss into a permanent financial mistake.

The SIP Safety Net: Consistency Over Timing

Because of the fear associated with dumping large amounts of money into the market, many people prefer the Systematic Investment Plan (SIP).

An SIP is designed to completely remove human emotion and the stress of “timing the market.” Instead of investing everything at once, you invest a fixed, smaller amount on a specific date every month. When the market is crashing and prices are cheap, your monthly investment automatically buys more mutual fund units. When the market is booming and prices are expensive, it buys fewer units. Over time, this averages out your purchase cost.

If you use a sip calculator, you can see exactly how effective this is. Investing just ₹20,000 a month for 15 years at the same 12% return results in a total investment of ₹36,00,000, which grows into roughly ₹1,00,00,000 (One Crore). You build massive wealth, and because the money enters the market in small drips, you sleep peacefully at night.

But here is the catch: If you already have ₹15 Lakhs sitting in your bank today, you cannot just set up a ₹20,000 monthly SIP from your savings account. It would take you more than 6 years to fully deploy your cash. During those 6 years, the uninvested portion of your money would earn almost nothing in the bank, getting crushed by inflation.

The Strategic Bridge: The Systematic Transfer Plan (STP)

You do not have to choose strictly between the anxiety of a single large investment and the slow, dragging inefficiency of a standard monthly plan. There is a perfect middle ground. You can earn decent interest on your idle cash while still taking advantage of the safety and cost-averaging of an SIP.

This hybrid strategy is called a Systematic Transfer Plan (STP). Here is exactly how you execute it:

- Park the Cash Safely: Instead of leaving your ₹15 Lakhs in a standard savings account earning 3%, move the entire amount into a Liquid Mutual Fund or an Arbitrage Fund. These are incredibly low-risk funds that do not invest in volatile stocks. They invest in safe, short-term government and corporate debt. They generally provide steady, bank-like returns (often around 6% to 7%).

- Automate the Transfer: Once your money is parked in the liquid fund, you set up an automated instruction with the mutual fund house. You tell them to automatically move a fixed amount—let’s say ₹1 Lakh—out of the safe liquid fund and into a high-growth equity mutual fund on the 5th of every month.

- The Final Result: Your bulk money stays safe and earns better-than-savings-account interest. Meanwhile, ₹1 Lakh enters the volatile stock market every month. If the market crashes, your automated transfer buys equity units at a massive discount.

Using Both Calculators to Map Your Plan

To see exactly how this strategy plays out, you must use both financial calculators to map the two different halves of your money.

First, use the lumpsum calculator to understand the “safe” half of your strategy. You can project how much interest your parked capital will generate in the liquid fund over the 15 months it takes to empty out. Even though the capital is depleting every month, it is still earning interest on the remaining balance, keeping it highly productive.

Next, use the sip calculator to track the “growth” half of your strategy. Because you are shifting ₹1 Lakh into the equity fund every month, the equity side of your portfolio behaves exactly like a massive SIP. The calculator will show you how these regular, heavy transfers will compound over the next decade once they are fully deployed in the market.

By running both calculations, you get a clear, mathematical picture of your wealth. You successfully protect your downside risk, completely bypass the stress of timing the market, and ensure every single rupee is working for you.

Golden Rules for Executing This Strategy

If you decide to bridge your investments using this method, keep these practical rules in mind to avoid common mistakes:

- Keep the Timeline Tight: Do not drag your transfers out for five or ten years. If you take too long to move the money into equity, you defeat the purpose and lose out on market growth. A standard, highly effective timeframe for moving a large windfall into the market is spreading it across 12 to 24 months.

- Do Not Panic During Crashes: The entire mathematical advantage of this strategy is buying cheaper units when the market drops. If the stock market crashes by 15% halfway through your transfer plan, do not panic and cancel the automated transfers. That is exactly the moment the strategy is working hardest for you.

- Mind the Tax Rules: In India, moving money from a liquid fund to an equity fund is legally treated as selling the liquid fund and buying the equity fund. You may have to pay a small amount of tax on the interest earned in the liquid fund during the holding period. Always factor this into your net returns.

Conclusion

Investing a large amount of cash should feel empowering, not paralyzing. You do not need to gamble on the perfect entry point, nor do you need to let inflation destroy your savings in a bank account. By parking your money in a safe holding fund and trickling it into the market systematically, you get the absolute best of both worlds. Run your numbers, set up your automated transfers, and let the system do the heavy lifting while you get on with your life.

Happy

0 %

Sad

0 %

Excited

0 %

Sleepy

0 %

Angry

0 %

Surprise

0 %

More Stories

isCalculator Free Financial Tools: The Smart Way to Manage Your Money

Managing money used to mean expensive software, paid advisors, or a weekend lost to spreadsheets. Not anymore. Free financial tools...

Best Digital Gold App in India for SIP and Long-Term Investment

Ask any Indian family where their gold is, and the answer is almost always the same: the locker. A pair...

Best Demat Accounts for Long-Term Investors in 2026

To invest in the equity and commodity markets, an investor basically needs three key accounts Bank Account, Trading Account &...

The Future of Financial Content Management in an API-Driven World

Financial content management is changing quickly as financial services become more digital, connected, and customer-focused. Banks, insurance providers, investment firms,...

Why Multicap Funds from Nippon India Mutual Fund Are Gaining Attention Among Investors?

Most investors spend years wrestling with the same decision. Do they go all-in on large caps for safety? Chase mid...

How Small Businesses Can Leverage Crypto Search Trends for More Website Traffic

Small businesses recognize the difficulty of standing out online. Visibility is crucial for growth, but rising competition complicates it. A...